Cost Comparison Of Cross Border Fund Transfer Methods

·Pay to China & get paid globally

·Free to open business accounts

·24/7 instant payment

·Exchange USD/RMB, no limit, no block

Exchange Rate Converter

Register on the XTransfer website

Our customer service will provide one-on-one support

Upload with one click

Simple operation, no complicated process required

Ensure enterprise information security

The whole process is professional, efficient, transparent, and secure

Quickly start cross-border payments

Connect with banks in different countries worldwide

New user special:enjoy free settlement for ¥100,000!

Our Strength

24/7 RealTime Online Currency Exchange

Whether it's a holiday, weekend, or late at night, redeem anytime you want!

Constant Access to Market-Beating Rates

Enjoy secure and compliant exchange at competitive rates with 0 exchange loss

FX limit orders

Set limit orders and automatically exchange at your preferred rate

Hong Kong/Chinese mainland Company Registration

XTransfer connects you with licensed secretaries to register your company and activate global payment reception quickly and remotely.

Send Money to China, the Most Cost-Effective Choice

The Fastest & Easiest Way to Cost Comparison Of Cross Border Fund Transfer Methods

Partner

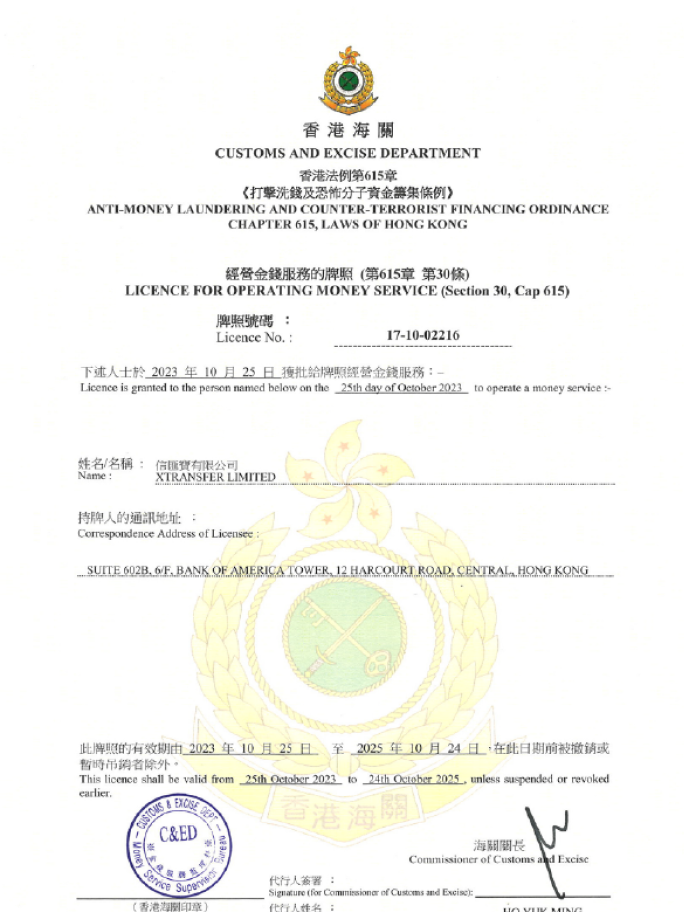

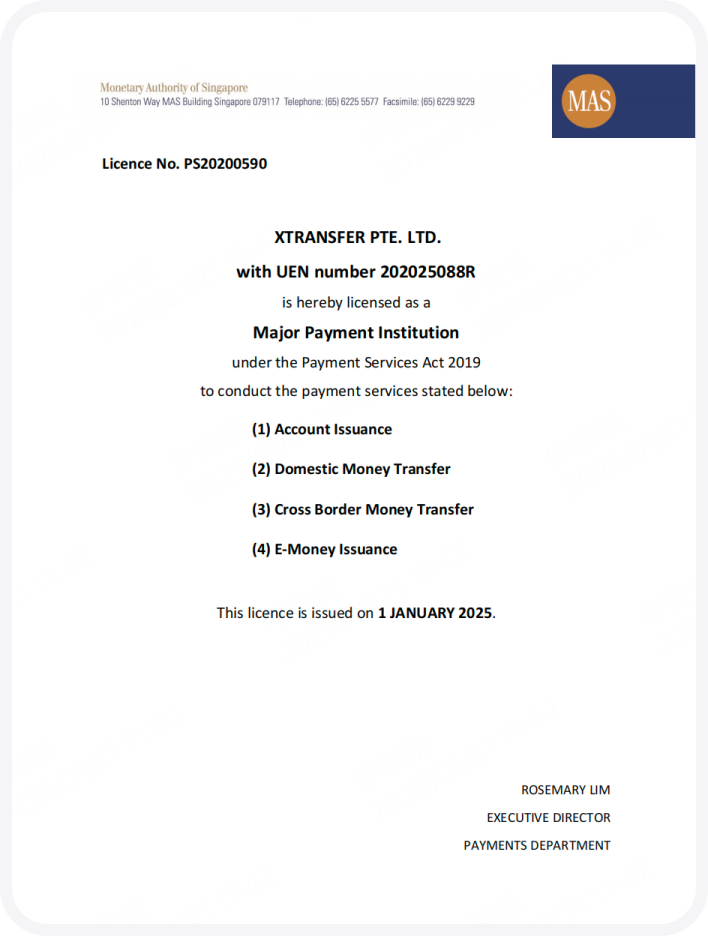

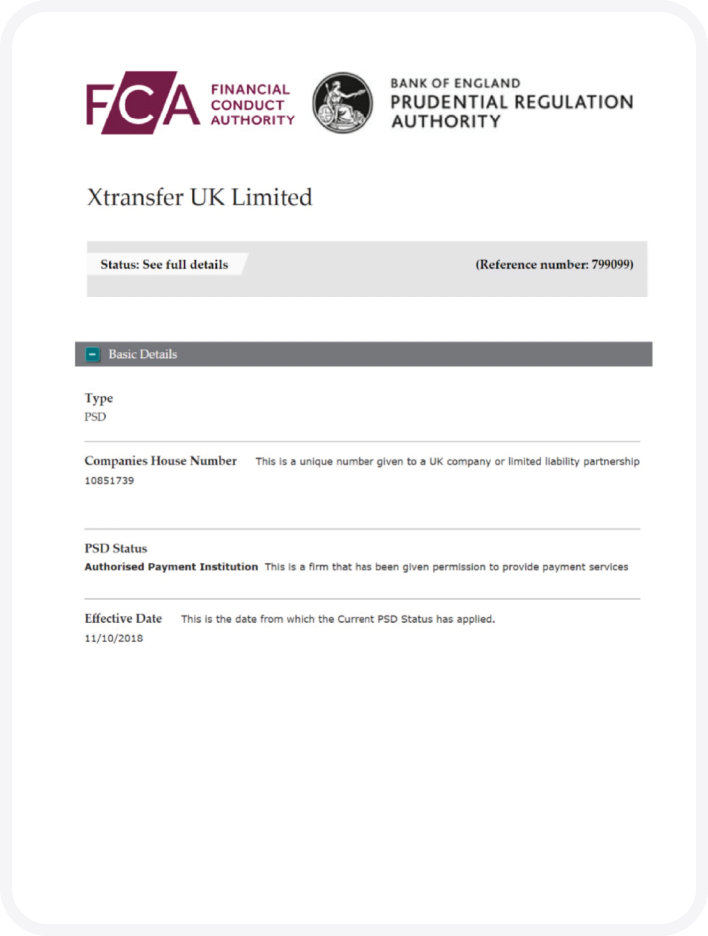

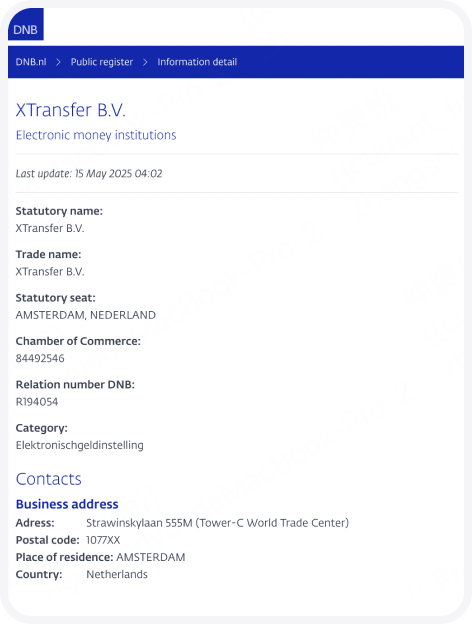

Our licenses

China

HK MSO License

Singapore

UK API License

Netherlands

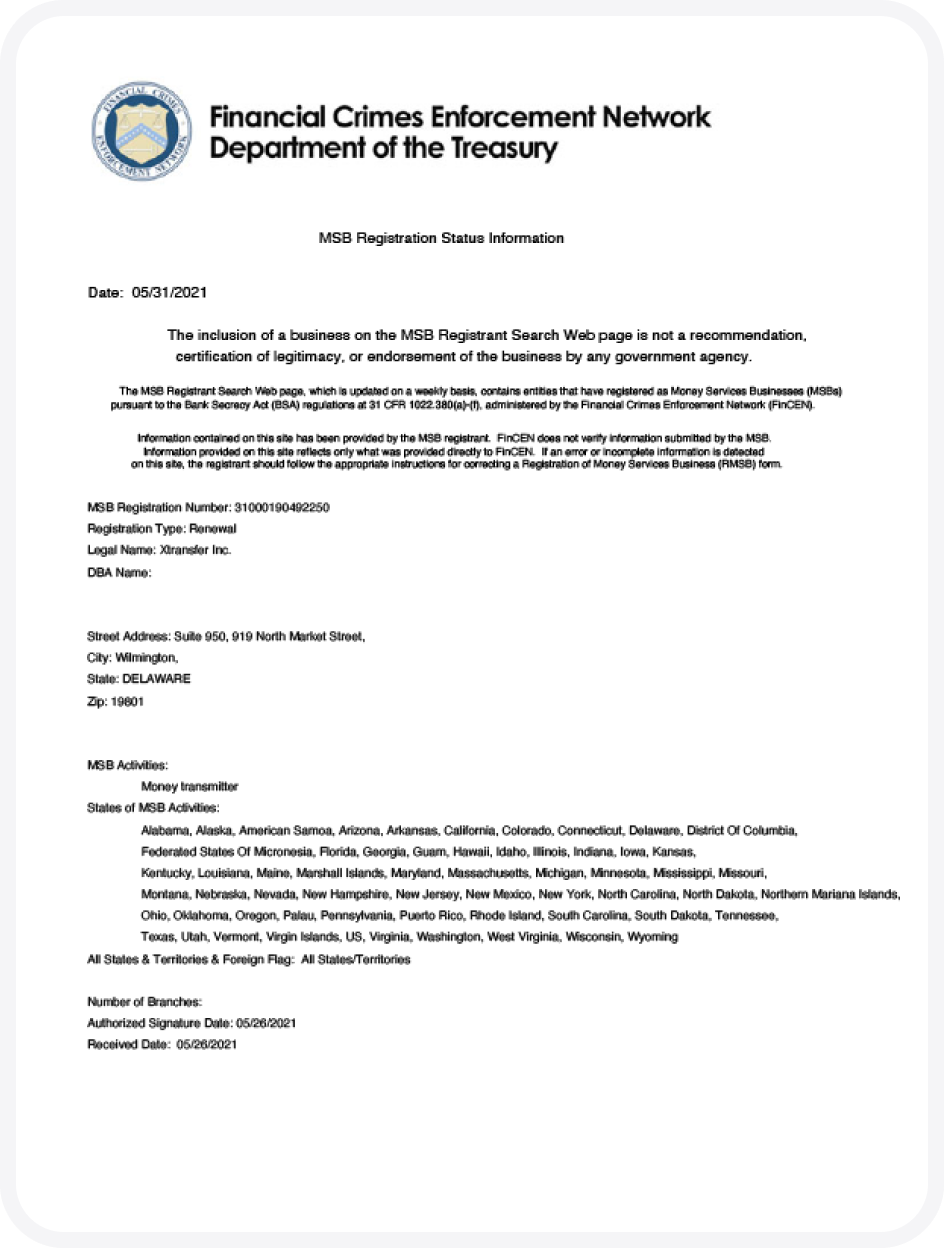

US MSB

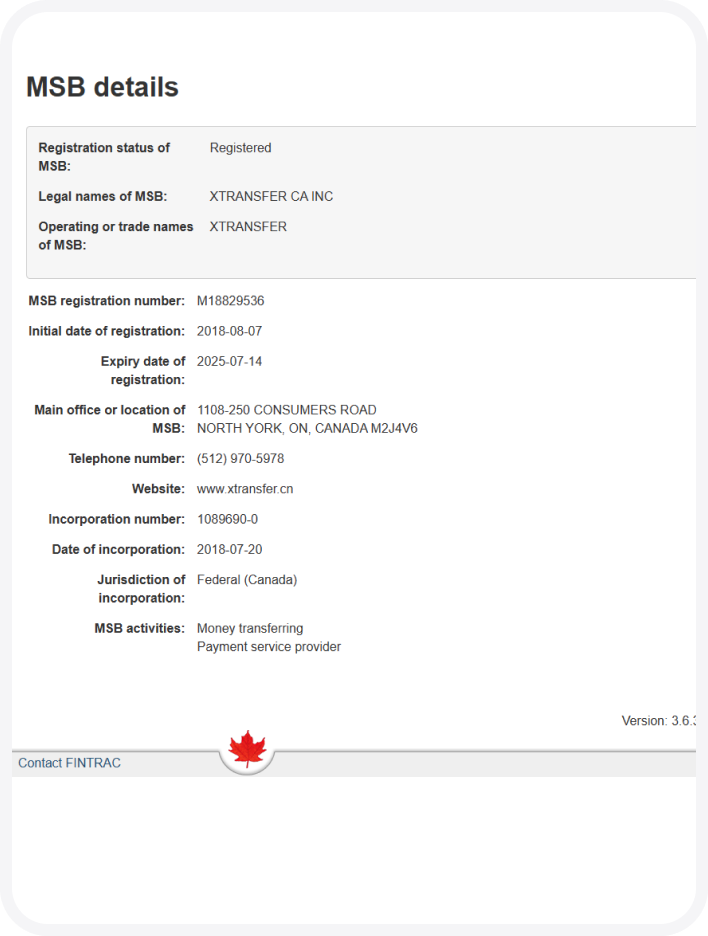

CA MSB

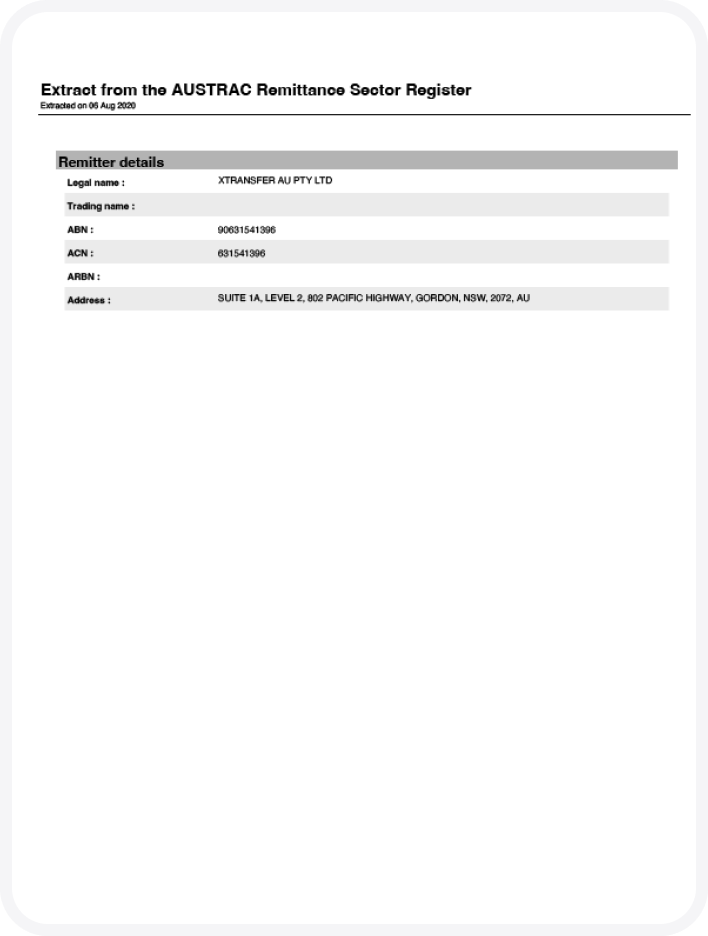

AU RSP

Cost Comparison Of Cross Border Fund Transfer Methods

Cross-border B2B settlement refers to the process by which foreign trade enterprises collect and convert foreign currency payments paid by overseas purchasers into their own currency. Efficient collection and settlement of foreign exchange is not only related to the speed of capital withdrawal, but also the key to the protection of corporate profits. With specialized B2B cross-border payment infrastructure such as XTransfer, companies can easily have global multi-currency collection capabilities. It not only supports fast and safe US dollar collection, but also enjoys a transparent and optimized exchange rate to help foreign trade enterprises move forward steadily in the complex and changeable international market and achieve cost reduction and efficiency increase.

Cross-Border Traders Around You

Are Using XTransfer

Grateful To Have You By Our Side

方便快捷!

很方便,出差可以手机操作

Confidently Secure System

We transact with peace of mind regarding security.

Perfect for Exporters

Receiving USD payments from international clients is now much easier.

The Best Decision I Made This Year

Switching to XTransfer was the best operational decision I made for my business. The ROI is incredible.

Helpful for Traders

Essential for our import/export business. The interface is functional but feels a bit out-dated and could use a refresh.

Exceptional Customer Support

Their support team is phenomenal. They resolve issues in minutes, not hours or days.

XTransfer at your fingertips

Facing the payment needs across different countries and currencies, XTransfer provides a unified collection and management solution, allowing businesses to complete major payment and settlement processes without repeatedly handling complex banking procedures. Whether for daily small payments or long-term multi-currency, multi-market trade settlements, XTransfer makes cross-border fund transfers more efficient, secure, and compliant.

Use the exchange rate calculator below to quickly understand the conversion relationships between different currencies, providing reference for payment and settlement decisions.